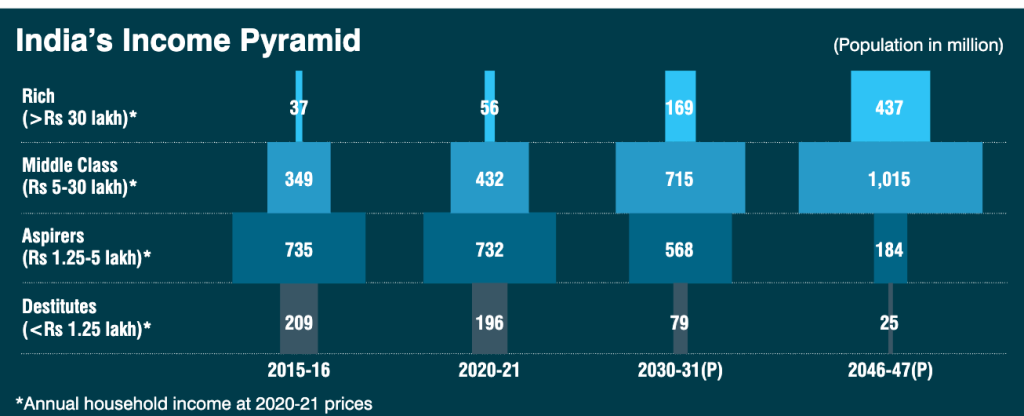

The recent survey conducted by PRICE1 states that India’s income pyramid can be spilt into four groups

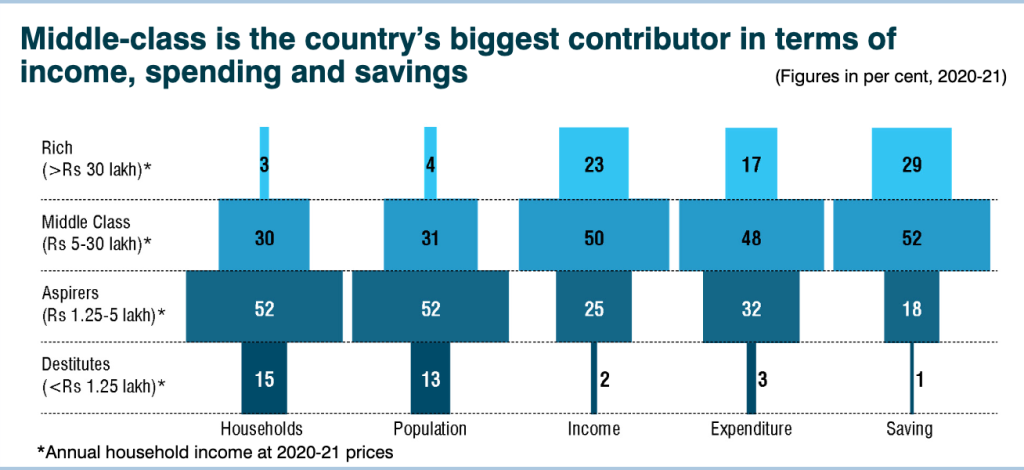

The report suggests that the middle class is the country’s biggest driver of income, spending, and savings. The rise of India’s middle class is real, and it is this section of the society that is shaping the modern Indian economy.

It can be seen that the biggest contributors for income, spending, and savings are from the middle class. However, the expenditure for the middle class is more driven by salaried income and self-employment income and not from the passive income sources like the investment income from the equities. In America, securities make up 59% of the household portfolios in North America, but in India, it is only 13%. In India, especially the salaried class, who make the bulk of the middle class has expenditure predominantly on home loan/personal loan EMI, health/life insurance, pension outgo, rental expenses, hospital care expenses and school fees with very little savings that is left at the end. It is here that tax incentives have played an extremely important aspects for the middle class to invest in mutual funds and other securities so that they get the dual advantage of a investment and also tax advantage.

Now the current day middle class has access to the mobile phone and the internet but does not have the access to the capital markets, especially the safer ones. It would be very unsafe to allow these population to equities wherein the price variations are huge.

However, to ensure better liquidity and reasonable returns on their investments, a model should be designed wherein micro investment products can be designed and also financial technology can be delivered in vernacular languages. Think of this mutual fund industry wherein a minimum ticket size of Rs 5000/- per month can encourage a large segment of the population to invest in this. Most of them can go till Rs 20000/- per month as we go higher. The Indian population is convenient with monthly tickets rather than the yearly outgo. Another important bottleneck for the middle class is that they are mostly involved in investment in gold, real estate, and savings in cash rather than parking that hard-earned money in some equity. This change in attitude can come only when there is community-based financial education delivered in various languages. This is currently a big bottleneck wherein the middle class does not know the benefits of investing in stock markets or mutual funds.

One of the biggest needs for the middle class is the short-term need of money for medical exigencies, marriage expenditure, and other expenditures at times. Now, for example, if a person has invested Rs 20000 per month for 2 years, he would have accumulated Rs 4.8 lakhs. Now let us assume that this fund has grown to maybe Rs 7.5 lakhs. Now the person should be allowed to take out or sell off his portfolio for at least 25%, with an intermediary managing all the transactions. This would ensure that more people would start using the equity route to meet their contingencies instead of taking short-term loans or taking credit cards, which is much more costly. One more of the biggest problems with the current middle class is their obsession with gold and real estate. It is here financial education becomes important and assured returns and wealth management become more important when helping this middle class manage their wealth.

Now with the UPI Ecosystem enabled, it is now possible for the government to directly get involved in enabling the middle class to invest in stock markets and ensure that their portfolios are handled in a systematic way. For example, if surplus funds are available in bank accounts, automatic suggestions that if you invest in FD, you will get this many returns, etc., would always motivate the middle class to invest in the safe assets.

A long road ahead is awaited. However India’s wealth inequality would reduce only when Indian middle class start investing in financial assets. The gap between Bharat and India can be reduced by fuelling middle class investment in safe, high quality financial assets.

That requires a strong government regulator and also financial inclusion models that needs to be built over and above the UPI Infrastructure.

Written By : Nethrapal IRS, Commissioner of Income Tax, New Delhi